06.10.2025

Reforming the System to End the Cycle of Unsustainable Federal Student Loan Debt

The federal government lends over $80 billion in student loans every year, yet the system too often fails those it was designed to help and continues to allow far too many students and families to overborrow to pay for higher education. Some federal student loans, which includes Graduate and Parent loans, are made in virtually unlimited amounts and without meaningful underwriting, often to students and parents who are not able to pay them back. This has contributed to overborrowing and the rising cost of higher education.

In addition, the system notoriously lacks transparency, ranging from admissions and selection criteria to the real cost of attendance, making it very difficult for families to comparison shop and make informed decisions.

Addressing these issues would bring long-lasting solutions that are good for students, parents, and the federal higher education system as a whole.

Three Recommendations for Reform

1. Address college costs and limit overborrowing

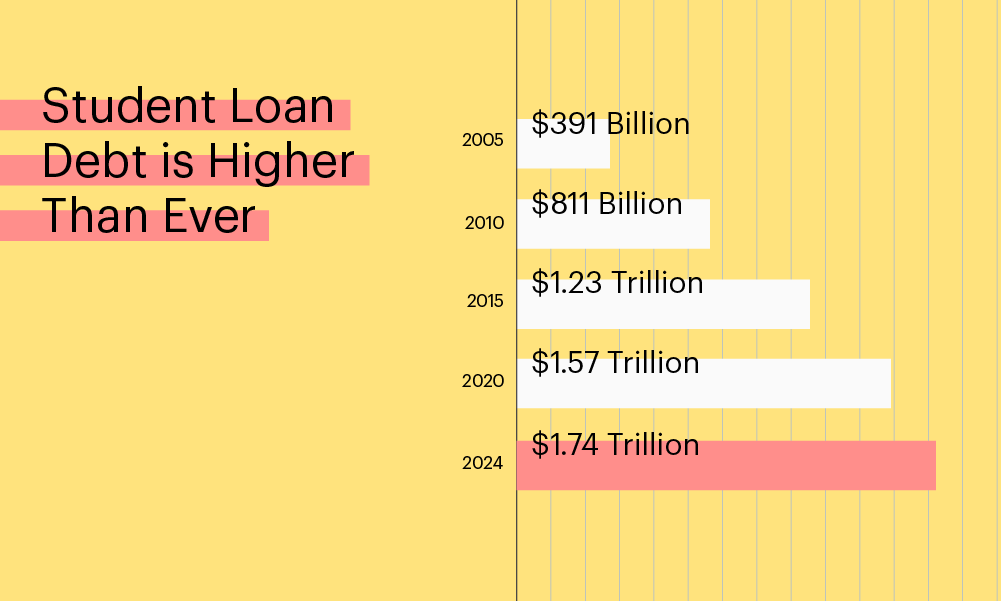

Americans hold roughly $1.74 trillion in student loan debt as of the second quarter of 2024. Of that total, roughly 93% are made by the government. The remaining 7% are private student loans, which are credit based and underwritten by private lenders, who assess ability to repay before making a loan.

One of the biggest drivers of unsustainable debt is the federal program’s allowance for near-unlimited borrowing—including loans to parents that largely do not assess their ability to repay. These loans now total more than $100 billion for more than 3 million families. Federal graduate lending has also exploded, adding another $100 billion more to the federal balance sheet, accounting for nearly half of all newly issued federal student loans.

These programs have been labeled ‘predatory’ from experts on both sides of the aisle, and polling confirms most Americans believe addressing the unlimitednature of federal loan programs will protect students, and make college more affordable.

By allowing virtually unlimited borrowing without considering the ability to repay, the federal program continues to create unsustainable debt levels and limits incentives to explore affordable education options. Putting reasonable limits on these federal loan programs would protect families from taking on more than they can afford to repay and encourage students to consider all educational options, bending the curve of rising college costs.

2. Focus resources on those who need the most support

Access to higher education remains uneven. The federal student loan program continues to do too much for too many and not enough for those who need the most support. Too often, students from underserved communities – many of whom are first-generation college students — lack the tools and resources needed to make well-informed, confident decisions about paying for their higher education.

Borrowing should never be the first option for paying for college, but the current federal financial aid system is poorly designed to avoid it. Pell Grants, once a cornerstone of college affordability for those who truly needed assistance, haven’t kept pace with rising tuition. They now cover less than 30 percent of the average cost at a four-year public university, down from nearly 80 percent in 1980. Redirecting resources to expand Pell Grants could boost enrollment and retention for students who show financial need. Increasing Pell Grants for those who need the most support is one of the most effective ways to reduce their reliance on borrowing and keep access to college within reach for more students.

We also need to make it easier for them to apply. In 2024, more than $4 billion in Pell Grants went unclaimed, money that could have put higher education within reach of students who need it most. Reforms to graduate lending could generate more than $40 billion in federal savings over the next decade. That’s funding that could be redirected to expand need-based aid and support for non-traditional and workforce-aligned programs—creating more pathways to success without unsustainable debt.

In addition, the issues that have plagued the Free Application for Federal Student Aid (FAFSA®) need to be fully addressed, so the already complex process of applying for federal financial aid is less confusing for students and families. Likewise, financial aid offers from schools should also be clearer and more transparent so that families understand the true cost of college and how much they will ultimately need to pay.

We offer all students and families access to free college planning tools including a free scholarship search tool, and step-by-step FAFSA guide.

3. Empower degree completion

Access to college on its own is not enough – higher education stakeholders need to focus attention and resources on prioritizing college completion just as much as college access.

Far too many students take on debt without earning a degree. In fact, more than 40 million Americans have some college education but no degree.

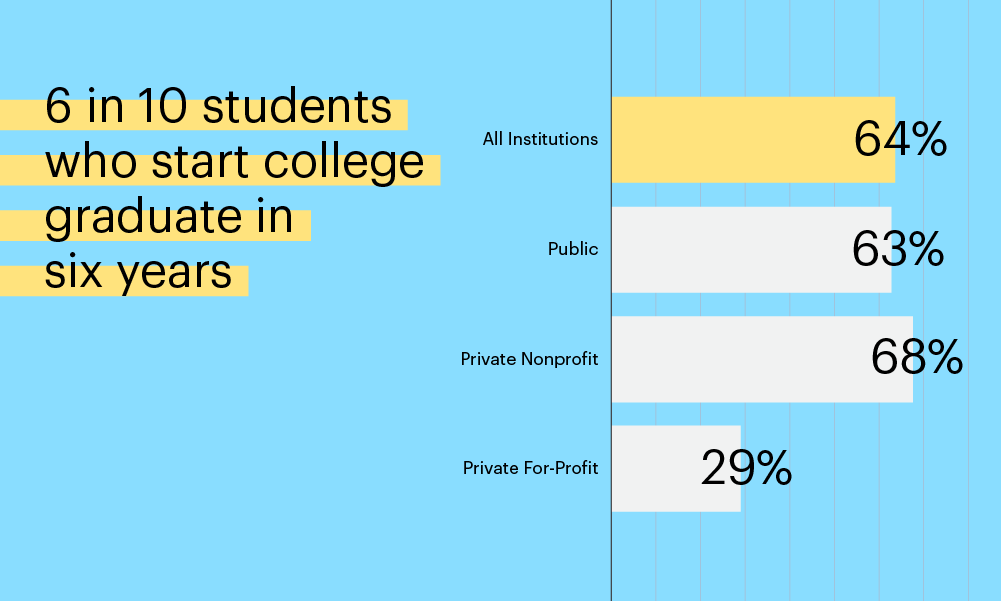

In addition, roughly six in 10 students who start college graduate in six years. Research consistently shows financial issues, life changes, and mental health concerns are some of the barriers that keep students from graduating

Often small debts, overlooked bills, or expenses get in the way of completion. To address that issue, we created our Completing the Dream Scholarship in partnership with Thurgood Marshall College Fund.

We’ve also partnered with Delaware State University (DSU) to help close the college completion gap. Our $1 million research endowment to DSU funds a comprehensive three-year “Persistence and Completion Pilot Program” to study and understand barriers to college completion and help students return to school to complete their degrees. The research will help advance policy recommendations and best practices that enhance student re-engagement at DSU and other institutions nationwide.

Without meaningful reform to curb overborrowing, the cost of college will keep rising, another generation of students will keep taking on unaffordable debt, and taxpayers will continue footing the bill. Reforming the system and addressing the cycle of ever-growing federal student loan debt will require collaboration among higher education leaders and stakeholders. Sallie Mae is committed to driving meaningful change by promoting a more transparent federal student aid system.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability