Author: tsmadmin

03.03.2026

Who Sallie Mae Is — and Isn’t

We promote responsible borrowing and advocate for policies and solutions that support higher education access, affordability, and completion.

The Sallie Mae® of today might surprise you. We’re not part of the federal government or a federal student loan servicer. We provide students and families with free college planning resources and responsible private student loans to cover any gaps in financing after income and savings, scholarships, grants, and other federal financial aid.

Investing in Student Success

Sallie Mae provides free planning tools and resources help students and families understand their options, compare costs, find scholarships, and make more informed decisions. Last year, more than 5 million students and families accessed these free resources.

These free tools and resources include:

- Scholly Scholarship Search which helps connect students to scholarships based on their skills and interests.

- Scout College Search which helps students explore and compare colleges based on what matters most to them – like majors, location, and cost – so they can find the right school.

- A step-by-step guide to completing the Free Application for Federal Student Aid (FAFSA)

- Industry leading research on paying for college, college completion, and success after college.

- Scholarship programs like Bridging the Dream for High School Seniors, Completing the Dream, and Bridging the Dream for Grad School that help more students access and complete their education.

- Free calculators and resources to help families budget, estimate college costs, and navigate repayment.

Sallie Mae’s Approach to Lending

Private loans, like those offered by Sallie Mae, make up roughly 8% of loans today. The remaining 92% of loans outstanding are made by the federal government. If a student does need to borrow – and roughly half do – Sallie Mae believes they should borrow only what they need and what they can reasonably afford to repay.

To that end, Sallie Mae embeds a broad set of customer protections in the products that it offers. Sallie Mae conducts a thorough assessment of the customer’s ability to repay the debt – a feature that goes beyond what is available in the federal loan program. To ensure students borrow only what they need to cover their cost of attendance, Sallie Mae actively engages with schools and requires school certification before disbursing a loan. To help students understand their loan terms, Sallie Mae provides multiple, customized disclosures that include the interest rate, whether the interest rate is fixed or variable, and an estimate of the loan’s total cost. Requiring these same disclosures across federal student lending programs would give families clear, comparable information.

This disciplined approach is working. Sallie Mae customers typically pay back their loans in 6-7 years and fewer than 3% of loans in repayment default annually.

Sallie Mae also recognizes that, for some students, a loan is simply not the right answer. That’s why the company continues to advocate broader reforms including meaningfully expanding Pell grants and opportunities for low-income students, making financial aid offers easier to compare, providing more access to scholarships, and simplifying the credit transfer process to boost college completion.

Higher education remains one of the most important investments a family can make. It works best when the system is transparent, accountable, and focused on outcomes. Our work is grounded in that belief, and it’s why we advocate for policies that help make the higher education system work better for students and families.

FAFSA is a registered service mark of U.S. Department of Education, Federal Student Aid

Related Posts

How America Pays for College 2025

Education Landscape, Financial Literacy

01.28.2026

Government Study Reveals Need for Clearer College Financial Aid Offer Letters

A Government Accountability Office report confirms inconsistent financial aid offer letters from colleges and universities leave families without a clear understanding of the true cost of higher education—strengthening the case for clearer, standardized requirements.

A study by the federal Government Accountability Office (GAO) found that 91% of colleges and universities understated or failed to include a clear net price — the amount a student pays after scholarships and grants — in their financial aid offer letters. In addition, many financial aid offers don’t itemize costs such as tuition, fees, housing, books, and transportation, which leads to surprise expenses for families and makes budgeting difficult.

Colleges and universities send these “award” letters to accepted students each year, and for the nearly 75% of undergraduates receiving some form of financial aid, they are often the primary source of information families rely on to understand affordability and make enrollment decisions.

Despite their importance, there is currently no standard format for how financial aid information is presented. Colleges use different terminology, layouts, and assumptions, leaving families to decipher complex financial information on their own and making it difficult to compare offers across institutions. Clearer, more consistent requirements would help ensure families receive the information they need during such a critical moment. Establishing a standard offer letter would be a good step toward providing clarity and transparency.

Hidden Costs

The same GAO study found some offer letters do not clearly identify funds that need to be repaid, such as federal student loans. In many cases, institutions subtract Parent PLUS loans – federal loans made to parents with minimal credit checks – from the total cost of attendance.

The report notes just how misleading this can be: “Subtracting this type of loan from the cost of attendance can drastically underestimate the amount a student’s family will need to pay for college.”

Taken together, it’s much more difficult for families to make informed financial decisions without a complete view of the costs they will actually pay.

Reform Is Needed

The report concluded that “further congressional action would be necessary to ensure that students receive the information they need in their financial aid offers to make informed education and financial choices.”

This reflects growing recognition that clearer, more consistent requirements are needed to bring transparency and comparability to the presentation of how financial aid information. Policy efforts focused on standardizing financial aid offer letters seek to make sure families receive clear, plain-language information across institutions, including a clearly stated net price, itemized costs, and transparent distinctions between grants and loans.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

How America Pays for College 2025

Education Landscape, Financial Literacy

09.04.2025

How America Pays for College 2025

Education solutions company and responsible private lender Sallie Mae and research firm Ipsos® recently released its annual research report, How America Pays for College , providing key insights into how current undergraduate students and parents of undergraduates view higher education and how they plan and pay for it. This industry-leading research considers education funding sources — from parent and student income and savings to scholarships, grants, and borrowed funds — while evaluating trends in college spending over time.

Surveyed

1,000 parents of undergraduate students (ages 18–24)

1,000 undergraduate students (ages 18–24)

College Spending Increases

Undergraduate families reported spending an average of $30,837 on higher education for the academic year 2024-25 — a 9% increase from last year’s $28,409. This year’s spending is more in line with 2019–20, pre-pandemic, when families spent an average of $30,017 on college.

Families relied on income and savings to cover nearly half (48%) of costs, followed by scholarships and grants (27%), borrowing (23%), and contributions from family or friends (2%).

Families See Value in College but Remain Cost-Conscious

Nearly nine in ten families (89%) said college is a worthwhile investment, and 82% are willing to stretch their finances to ensure the best opportunities for their students. At the same time, 79% reported eliminating at least one school based on cost. It’s also worth noting that 47% reported paying less than the sticker price for college.

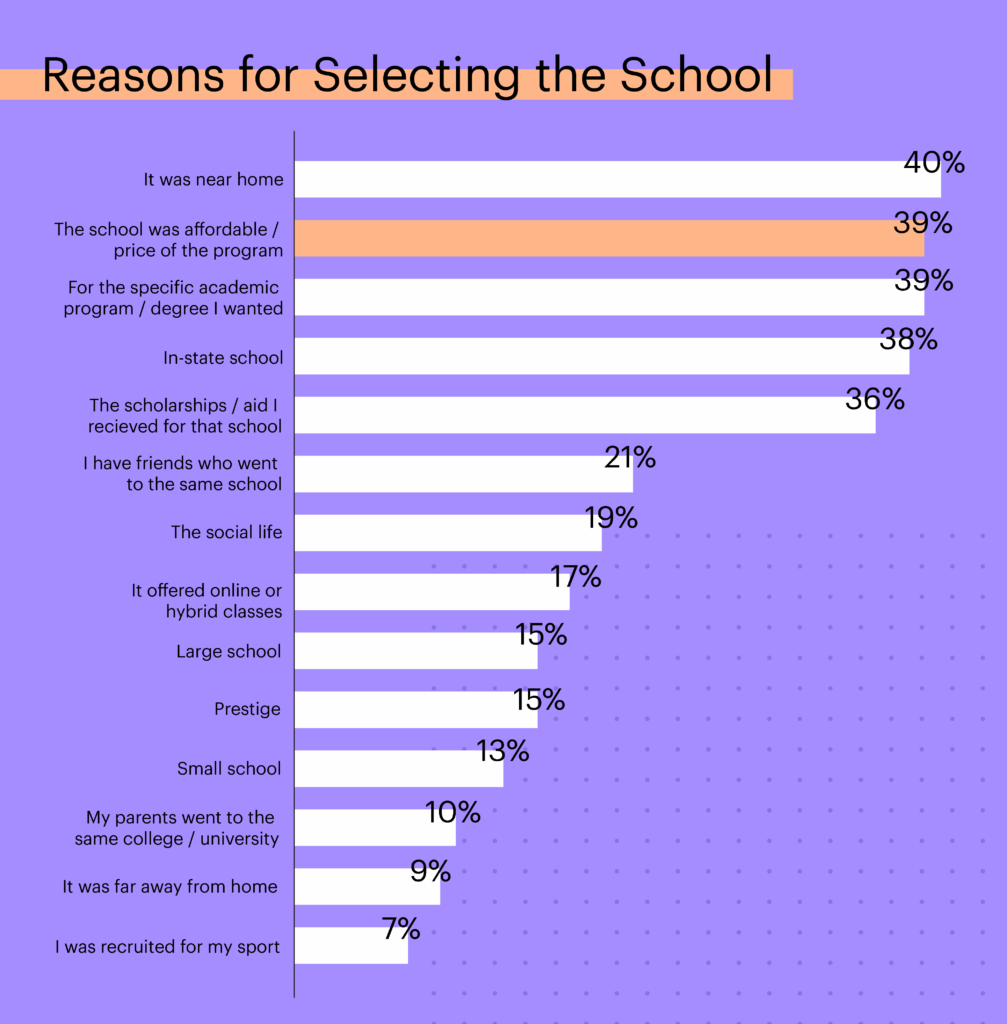

Families most often cited proximity to home (40%), affordability (39%), and specific academic program (39%) as top reasons for choosing a school. While 59% of families had a plan to pay for college before enrollment, just 38% considered starting salaries after graduation.

Key Resource: Find the right college for you

Scout College Search by Sallie® is a free and easy way to explore and compare schools based on location, majors, extracurriculars, and more.

Misconceptions About Scholarships Persist

Scholarships remain a valuable tool to help students and families access higher education. Families who received scholarships reported an average of $8,004 in funding, and 75% said scholarships made it possible for the student to attend college.

Still, misconceptions about scholarships discourage some families from applying. Nearly half of families (46%) believe scholarships are only for students with exceptional grades or abilities, 34% didn’t apply because they didn’t think there were scholarships for them, and 32% assumed it wasn’t worth applying if their family earned “too much.” Another 36% mistakenly thought students could only apply before freshman year.

Key Resource: Search for scholarships

Find free money for college with Scholly® Scholarships by SallieSM, our free tool that connects students and families to thousands of scholarships–no signup required

FAFSA® Completion Declines Despite Easier Form

In academic year 2024–25, the first year that the updated FAFSA was rolled out, 71% of families submitted the application, down from 74% in 2023–24, despite 64% saying the new form was easier to complete.

Confusion remains: only 21% of families knew the FAFSA opens in October.

Families are also looking for clearer, more consistent financial aid communications. Two-thirds (66%) support standardizing financial aid offers to make them easier to compare, suggesting strong demand for clearer, more transparent communication around college costs.

Key Resource: Fill out the FAFSA® with our step-by-step guide

Everything students and families need to get ready for the FAFSA, including a free step-by-step guide that breaks down every question.

Access to Loans Leads Some Families to Reach for Higher-Priced Schools

Nearly half of families (48%) borrowed to help pay for college, and 72% of all families said they would rather borrow than miss out on attending. Roughly six in 10 families (59%) said the availability of federal student loans has driven up college costs, and more than a third (35%) of families said loan availability led them to consider more expensive schools. In addition, two-thirds of families (67%) said they support limits on how much federal student loan debt students can take on.

Key takeaways:

This year’s How America Pays for College findings underscore the importance of early planning and starting the higher education journey with outcomes in mind—considering the full picture of education costs and career paths. It also further highlights that many families still miss critical steps that could improve both college affordability and post-graduation success. More broadly, it illustrates the need for more transparency related to college costs, stronger awareness of available aid, and clearer communication around borrowing.

Download the full How America Pays for College 2025 report at SallieMae.com.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

by Nicolas Jafarieh, EVP, Sallie Mae | 06.10.2025

The Federal Government Allows Students and Families to Overborrow to Pay for College. It’s Time to Put an End to It.

The great promise of higher education has always been grounded in opportunity, personal and professional growth, and upward social mobility. Earning a degree equips students with the skills to compete in an evolving economy, increases lifetime earnings, and creates lasting multi-generational impact, especially for those from economically disadvantaged households.

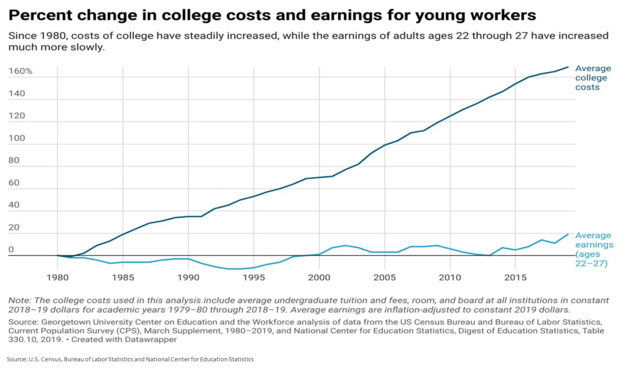

Looking at lifetime earnings alone, the value of a higher education for the vast majority of Americans is undeniable. Sadly, these benefits are slipping away for too many. The cost of attendance is rising more rapidly than wages for college graduates, squeezing the “return on investment” for a degree. Since 2000, tuition at public four-year institutions has surged nearly 180 percent.

SOURCE: U.S. Census, Bureau of Labor Statistics and National Center for Education Statistics

Institutional spending on administrative expansion, facilities, and non-academic programs has led to an ‘arms race’ among schools with costs passed along to students and families, many of whom already struggled to make college affordable. The system also notoriously lacks transparency, ranging from admissions and selection criteria to the real cost of attendance, making it very difficult for families to comparison shop and make informed decisions.

A System That Fuels Rising Costs

The federal loan program, originally designed to provide better access to higher education, has made college less affordable, and ushered in an age of overborrowing. Each year, the government lends more than $80 billion to students and families. Over the last two decades, loan limits have gone up and the federal government allows students and families to borrow more and more, much of it without ever assessing their ability to repay this debt. The Federal Reserve Bank of New York found much of the increases in loan limits directly translated to tuition increases. And these tuition increases, in turn, are forcing students and families to borrow even more.

Federal Graduate and Parent loans are made in virtually unlimited amounts, and again, without any meaningful assessment of the borrower’s ability to repay them. This unconscionable practice has no equivalent anywhere in the financial world. The impact has been staggering. Today, 3.6 million families owe collectively more than $100 billion in Parent PLUS loans. Federal graduate lending has exploded, adding another $100 billion more to the federal balance sheet, accounting for nearly half of all newly issued federal student loans. These programs have been labeled ‘predatory’ from experts on both sides of the aisle, and polling confirms most Americans believe addressing the unlimited nature of federal loan programs will protect students, and make college more affordable. According to the Committee for a Responsible Budget, reforms to graduate lending alone could generate over $40 billion in savings over the next decade—money that could be used to expand Pell grants and need-based aid.

Redirecting Resources to Those Who Need Them Most

Pell Grants, once a cornerstone of college affordability for those who truly needed assistance, haven’t kept pace with rising tuition. They now cover less than 30 percent of the average cost at a four-year public university, down from nearly 80 percent in 1980. Meanwhile, partly the result of missteps like the recent FAFSA delays, more than $4 billion in Pell Grants went unclaimed last year— money that could have helped students who need it most. Increasing Pell Grants for those who need the most support is one of the most effective ways to reduce their reliance on borrowing and keep access to college within reach for all Americans.

Allowing students to use grant aid on non-traditional programs, including short-term job training or apprenticeships, would help more individuals find a long-term path to professional and financial success. A traditional 4-year college continues to be attractive for most, but it is not the right answer for everyone.

Fixing the system, however, isn’t just about shifting resources, it’s also about transparency and ensuring families can make informed choices. College admission is stressful, and offer letters compound the problem. Financial aid offers should be clear, standardized, and easy to compare, giving families the information to make responsible school selections and financial decisions. That is not the case today.

We also need to help more students complete their degree. The great promise of higher education comes not from earning a few credits but from walking across the graduation stage. According to the National Student Clearinghouse, the number of Americans who have some college experience but no degree has now reached a staggering 40 million. Sallie Mae has partnered with Delaware State University to study how near-completer students can be re-engaged and policy solutions that help them complete their degree.

The Need for Reform

By offering federal Graduate and Parent PLUS loans in virtually unlimited amounts, and without considering the borrower’s ability to repay them, the federal government continues to operate like a predatory lender that saddles families with unsustainable levels of debt. This isn’t a failure of students and families—it is a failure of policy. Without meaningful reform to curb overborrowing, the cost of college will keep rising, another generation of students will keep taking on unaffordable debt, and taxpayers will keep footing the bill.

The solutions exist. Now is the time to act.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

06.10.2025

Reforming the System to End the Cycle of Unsustainable Federal Student Loan Debt

The federal government lends over $80 billion in student loans every year, yet the system too often fails those it was designed to help and continues to allow far too many students and families to overborrow to pay for higher education. Some federal student loans, which includes Graduate and Parent loans, are made in virtually unlimited amounts and without meaningful underwriting, often to students and parents who are not able to pay them back. This has contributed to overborrowing and the rising cost of higher education.

In addition, the system notoriously lacks transparency, ranging from admissions and selection criteria to the real cost of attendance, making it very difficult for families to comparison shop and make informed decisions.

Addressing these issues would bring long-lasting solutions that are good for students, parents, and the federal higher education system as a whole.

Three Recommendations for Reform

1. Address college costs and limit overborrowing

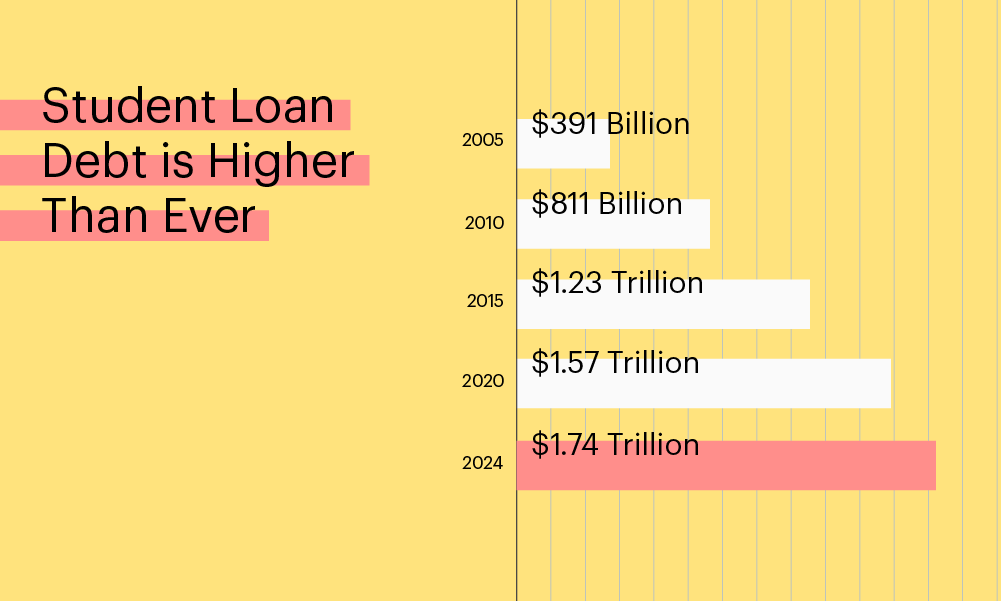

Americans hold roughly $1.74 trillion in student loan debt as of the second quarter of 2024. Of that total, roughly 93% are made by the government. The remaining 7% are private student loans, which are credit based and underwritten by private lenders, who assess ability to repay before making a loan.

One of the biggest drivers of unsustainable debt is the federal program’s allowance for near-unlimited borrowing—including loans to parents that largely do not assess their ability to repay. These loans now total more than $100 billion for more than 3 million families. Federal graduate lending has also exploded, adding another $100 billion more to the federal balance sheet, accounting for nearly half of all newly issued federal student loans.

These programs have been labeled ‘predatory’ from experts on both sides of the aisle, and polling confirms most Americans believe addressing the unlimitednature of federal loan programs will protect students, and make college more affordable.

By allowing virtually unlimited borrowing without considering the ability to repay, the federal program continues to create unsustainable debt levels and limits incentives to explore affordable education options. Putting reasonable limits on these federal loan programs would protect families from taking on more than they can afford to repay and encourage students to consider all educational options, bending the curve of rising college costs.

2. Focus resources on those who need the most support

Access to higher education remains uneven. The federal student loan program continues to do too much for too many and not enough for those who need the most support. Too often, students from underserved communities – many of whom are first-generation college students — lack the tools and resources needed to make well-informed, confident decisions about paying for their higher education.

Borrowing should never be the first option for paying for college, but the current federal financial aid system is poorly designed to avoid it. Pell Grants, once a cornerstone of college affordability for those who truly needed assistance, haven’t kept pace with rising tuition. They now cover less than 30 percent of the average cost at a four-year public university, down from nearly 80 percent in 1980. Redirecting resources to expand Pell Grants could boost enrollment and retention for students who show financial need. Increasing Pell Grants for those who need the most support is one of the most effective ways to reduce their reliance on borrowing and keep access to college within reach for more students.

We also need to make it easier for them to apply. In 2024, more than $4 billion in Pell Grants went unclaimed, money that could have put higher education within reach of students who need it most. Reforms to graduate lending could generate more than $40 billion in federal savings over the next decade. That’s funding that could be redirected to expand need-based aid and support for non-traditional and workforce-aligned programs—creating more pathways to success without unsustainable debt.

In addition, the issues that have plagued the Free Application for Federal Student Aid (FAFSA®) need to be fully addressed, so the already complex process of applying for federal financial aid is less confusing for students and families. Likewise, financial aid offers from schools should also be clearer and more transparent so that families understand the true cost of college and how much they will ultimately need to pay.

We offer all students and families access to free college planning tools including a free scholarship search tool, and step-by-step FAFSA guide.

3. Empower degree completion

Access to college on its own is not enough – higher education stakeholders need to focus attention and resources on prioritizing college completion just as much as college access.

Far too many students take on debt without earning a degree. In fact, more than 40 million Americans have some college education but no degree.

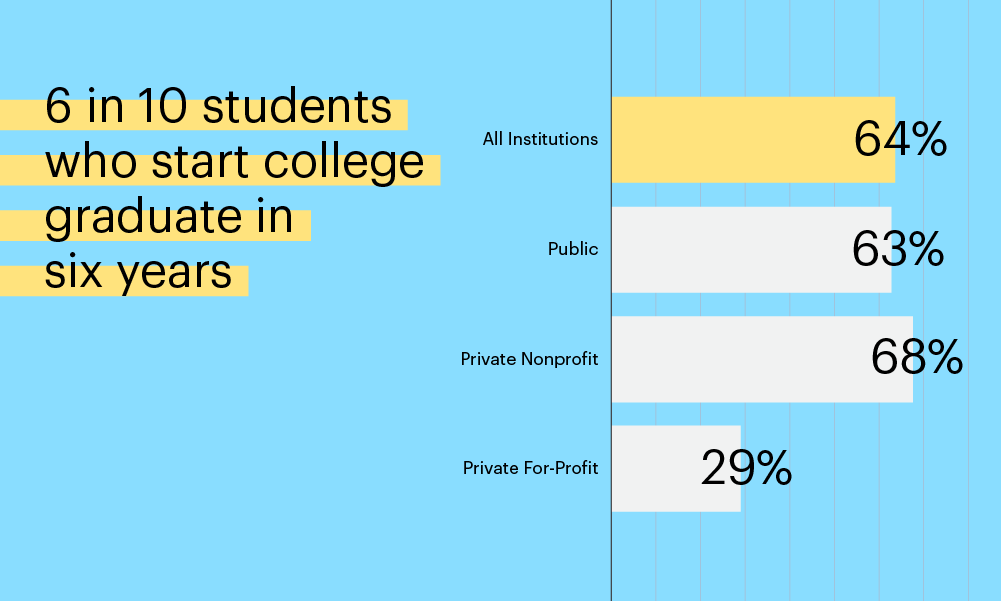

In addition, roughly six in 10 students who start college graduate in six years. Research consistently shows financial issues, life changes, and mental health concerns are some of the barriers that keep students from graduating

Often small debts, overlooked bills, or expenses get in the way of completion. To address that issue, we created our Completing the Dream Scholarship in partnership with Thurgood Marshall College Fund.

We’ve also partnered with Delaware State University (DSU) to help close the college completion gap. Our $1 million research endowment to DSU funds a comprehensive three-year “Persistence and Completion Pilot Program” to study and understand barriers to college completion and help students return to school to complete their degrees. The research will help advance policy recommendations and best practices that enhance student re-engagement at DSU and other institutions nationwide.

Without meaningful reform to curb overborrowing, the cost of college will keep rising, another generation of students will keep taking on unaffordable debt, and taxpayers will continue footing the bill. Reforming the system and addressing the cycle of ever-growing federal student loan debt will require collaboration among higher education leaders and stakeholders. Sallie Mae is committed to driving meaningful change by promoting a more transparent federal student aid system.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

05.13.2025

Supporting Students from Dream to Degree: Sallie Mae’s Commitment to College Completion

In 2023, Sallie Mae underscored its commitment to closing the college completion gap with a $1 million research endowment to Delaware State University (DSU). The grant supports a “Persistence and Completion Pilot Program,” that identifies and studies barriers to degree completion, helps students return to school, and develops policy recommendations and best practices so students can re-engage at institutions across the country. To date, the program has re-enrolled 213 students — nearly half of them first-generation college students.

This is important work. The number of students who have some college experience, but no degree, is over 40 million. Approximately 3 million are “near completers” who have stopped out mere credits away from degree completion.

Two near completer students — Nataniel (Tannie) Speaks and Chris Kearney — are proof of what’s possible when students get the right support at the right time.

After earning an associate degree, Tannie hoped to continue her education — but full-time work and raising two children put that goal on hold. Years later, she learned about the near completer program and re-enrolled at DSU. Five months later, she earned her bachelor’s degree.

“I still get chills and tears just thinking about it,” she said.

Chris’ journey also spanned decades. He first enrolled at DSU in 2000 with plans to earn a history degree, but stepped away in 2005 to support his growing family. A decade later, when his mother was diagnosed with breast cancer, Chris was determined to finish school for her. But after her passing, he once again put his education on hold.

In 2022, Chris felt a renewed urgency. “I’d reached a certain point in my career path where I felt the need to have my degree completed,” he said. “I thought it would complete me more holistically and professionally.”

In 2023, he graduated with a degree in liberal studies — this time, with his wife, siblings, and children cheering him on. “It felt like I was showing and giving examples to my children about fortitude and perseverance, about how sometimes when life happens, you can transcend, you can overcome and you can change the trajectory of your life for the better,” Chris said.

For Tannie, the impact of earning her degree was immediate.

“I want everybody—kids, young people, old people—to know that it’s never too late to finish your education,” Tannie said. “It’s a second chance at making something new.”

“Reach out to Sallie Mae. They have resources, they have things at their disposal to help encourage you to come back, and not only encourage you to come back, help you see this through to the end of your journey, ” Chris said. “You can do it. You have the wherewithal. You have the grit. Get it done.”

Sallie Mae is committed to supporting college completion. Too many students leave school just a few credits shy of a degree — often due to financial strain or personal circumstances. In fact, our 2024 “How America Completes College” report found that nearly half of non-completer said financial challenges played a role n their decision to leave school. Through programs like the “Persistence and Completion Pilot Program” at Delaware State University — and our “Completing the Dream Scholarship” — we’re helping remove barriers and support more students from dream to degree.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

11.22.2024

FAFSA: The Quiz

Each year, millions of students and families begin planning for college by completing the Free Application for Federal Student Aid (FAFSA®). It’s the gateway to accessing more than $100 billion in grants, scholarships, and other federal financial aid for higher education. Confusion and misconceptions about the FAFSA, however, persist — leading those who need the most support to potentially miss out on critical aid to make college more accessible and affordable. As an education solutions company and responsible private lender, Sallie Mae helps students and families complete the FAFSA, offering a free step-by-step guide as well as free resources to connect them to scholarships.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

11.22.2024

Why Scholarships are Critical for Families Paying for College

Paying for college can be a complex, stressful process. Yet, a new study finds students and families may be missing out on scholarships, which can help make college more accessible and affordable. In fact, 40% of families did not utilize scholarships to help cover college costs for the 2024-2025 academic year, according to Sallie Mae’s 2025 How America Pays for College report conducted by Ipsos.

In addition, misconceptions about scholarship availability and eligibility persist. More than half of families (52%) believe scholarships are only available for students with exceptional grades or abilities, and families who didn’t apply cited lack of awareness, doubt in winning, and effort required to apply. Families who didn’t apply cited lack of awareness (34%), doubt in eligibility (28%), and the effort required to apply as barriers.

The good news is there are free resources that can help connect students and families to scholarships. Scholly Scholarships easily finds and sorts through hundreds of available scholarships with no registration required.

Don’t Leave Free Money on the Table

Applying for free money is the first step in Sallie Mae’s 1-2-3 approach to paying for college.

Free money, such as scholarships and grants, are often what helps students from underserved communities access and complete higher education.

To help increase access and completion for more students, Sallie Mae’s Bridging the Dream Scholarship Program helps those from underserved communities access and complete college. Since 2021, Sallie Mae has awarded over 1,100 scholarships worth over $4 million in partnership with Thurgood Marshall College Fund (TMCF) through the Bridging the Dream Scholarship programs, which also include the Completing the Dream Scholarship and the Bridging the Dream Scholarship For Graduate Students. These scholarships are part of the company’s continued mission to help students access and complete higher education.

Connecting students with scholarships and grants before they borrow is critical. However, more clarity around college costs and greater transparency in federal lending programs would go a long way in helping families make informed decisions about higher education financing.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

11.01.2024

Sallie Mae Awards $400,000 in Scholarships to Increase Access to Higher Education

To celebrate National Scholarship Month, Sallie Mae announced the latest recipients of its Bridging the Dream Scholarship for High School Seniors. For the fourth consecutive year, The Sallie Mae Fund has awarded deserving students up to $10,000 each in scholarships to support their higher education goals pursuing a diverse range of degrees, including business, engineering, fine arts, humanities, and more.

Since 2021, Sallie Mae has awarded over 900 scholarships worth nearly $4 million in partnership with Thurgood Marshall College Fund through the Bridging the Dream Scholarship programs, which also include the Completing the Dream Scholarship and the Bridging the Dream Scholarship For Graduate Students. These scholarships are part of the company’s continued mission to help students access and complete higher education—especially those from underserved communities.

Applying for scholarships is critical in helping students and families responsibly pay for higher education, and an important part of the planning process. In 2024, 88% of students attending HBCUs relied on scholarships and grants to cover the cost of college, according to our How America Pays for College 2024 report. In addition to the Bridging the Dream scholarships, Sallie Mae provides Scholarship Search by Sallie, a free resource that connects students and families to hundreds of scholarships, helping them navigate the process easily with no registration required.

Meet This Year’s Bridging the Dream Scholarship Recipients

Aeneas Moore

Hometown: Conyers, GA

School: Howard University

Major: Architecture & Design Studies

Alijah Dean

Hometown: Murfreesboro, TN

School: Tennessee Tech University

Major: Engineering

Amaya Morene

Hometown: Jacksonville, FL

School: Howard University

Major: Humanities

Amos Prince

Hometown: Schenectady, NY

School: Rochester Institute of Technology

Major: Mechanical Engineering

Aniyah Prescod

Hometown: Conyers, GA

School: Hampton University

Major: Architecture

Ashlie Kearns

Hometown: Fayetteville, FL

School: East Carolina University

Major: Computer Science

Bryson Long

Hometown: Eads, TN

School: University of Tennessee at Martin

Major: Cyber Security

Charity DeBrew

Hometown: Greensboro, NC

School: University of North Carolina Chapel Hill

Major: Music Performance

Chris Moore III

Hometown: Macon, GA

School: Howard University

Major: Music Performance

Darius Williams

Hometown: Baton Rouge, LA

School: Morehouse College

Major: Business

David McGowan

Hometown: Rockaway, NJ

School: Kean University

Major: Technology

David Riley

Hometown: Atlanta, GA

School: Morehouse College

Major: Business Administration

Devin Miller

Hometown: Dallas, TX

School: Prairie View A & M University

Major: Civil Engineering

Heaven Rowell

Hometown: Stoughton, MA

School: Howard University

Major: Business

Ihuoma Mgbahurike

Hometown: Arlington, TX

School: Howard University

Major: Communications

Imani Monday

Hometown: Los Angeles, CA

School: Howard University

Major: Fine Arts

Iyanna Whipple

Hometown: Columbus, OH

School: Howard University

Major: Business

Jada McClide

Hometown: Locust Grove, GA

School: Clayton State University

Major: Health Science

Jayden Locklear

Hometown: Huntersville, NC

School: University of North Carolina at Charleston

Major: Biology

Journi Robinson

Hometown: Crofton, MD

School: Spelman

Major: Humanities

Kaandis Mance

Hometown: St. Petersburg, FL

School: University of Miami

Major: Music in Flute Performance

Kennedi Leary

Hometown: Covington, GA

School: Florida A&M University

Major: Fine Arts

Kennedy McCormick

Hometown: Riverview, FL

School: North Carolina A&T State University

Major: Marketing

Kenneth Stevenson

Hometown: Lawrenceville, GA

School: Morehouse College

Major: Science

Lillian Richards Smith

Hometown: Ellicott City, MD

School: Spelman College

Major: Science

Malani Martin

Hometown: Hanover, MD

School: Winston-Salem State University

Major: Sports Management

Margaret Mirembe

Hometown: Somerville, MA

School: Winston-Salem State University

Major: Kinesiology

Matthew Major

Hometown: Tampa, FL

School: Spelman College

Major: Human Resource Management

Mayah Prelow

Hometown: Mesquite, TX

School: Grambling State University

Major: Nursing

Mayte Segura

Hometown: Providence, RI

School: Vassar College

Major: Undeclared

Mikalah Williams

Hometown: Dulles, VA

School: Spelman College

Major: Science

Mira Reynolds

Hometown: Raleigh, NC

School: North Carolina A&T State University

Major: Chemical Engineering

Otis Lofton

Hometown: Columbus, GA

School: Howard University

Major: Pre-Law

RanDaijah Prince

Hometown: Atlanta, GA

School: Howard University

Major: Biology

Rianna Mafnas

Hometown: Winnfield, LA

School: Southern University and A&M College

Major: Fine Arts

Ryhmin Rawls

Hometown: Philadelphia, PA

School: Morehouse College

Major: Pre-Psychology

Teyana Porter

Hometown: Pensacola, FL

School: Florida A&M University

Major: Psychology

Victoria Pettway

Hometown: Wheatley Heights, NY

School: Tuskegee University

Major: Engineering

Xochitl Poindexter

Hometown: North Hills, CA

School: Hampton University

Major: Liberal Studies

Yakouba Keita Jr.

Hometown: Stonecrest, GA

School: Morehouse College

Major: Engineering

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

09.04.2024

How America Pays for College 2024

Education solutions company and responsible private lender Sallie Mae and research firm Ipsos® released How America Pays for College 2024, which provides key insights into how current undergraduate students and parents of undergraduates view higher education and how they plan and pay for it. This industry-leading research considers education funding sources – from parent and student income and savings to scholarships, grants, and borrowed funds – and evaluates trends in payment strategies over time.

From planning to paying, learn how families are navigating their unique higher education journeys.

Surveyed:

- 1,000 parents of undergraduate students (ages 18-24)

- 1,000 undergraduate students (ages 18-24)

- 349 undergraduate students (ages 18-24) from Historically Black Colleges and Universities (HBCUs)

College Spending Holding Steady

Families reported spending $28,409 on average this past academic year – in line with $28,026 in 2022-23. Students attending HBCUs spent an average of $28,545 in the academic year 2023–24.

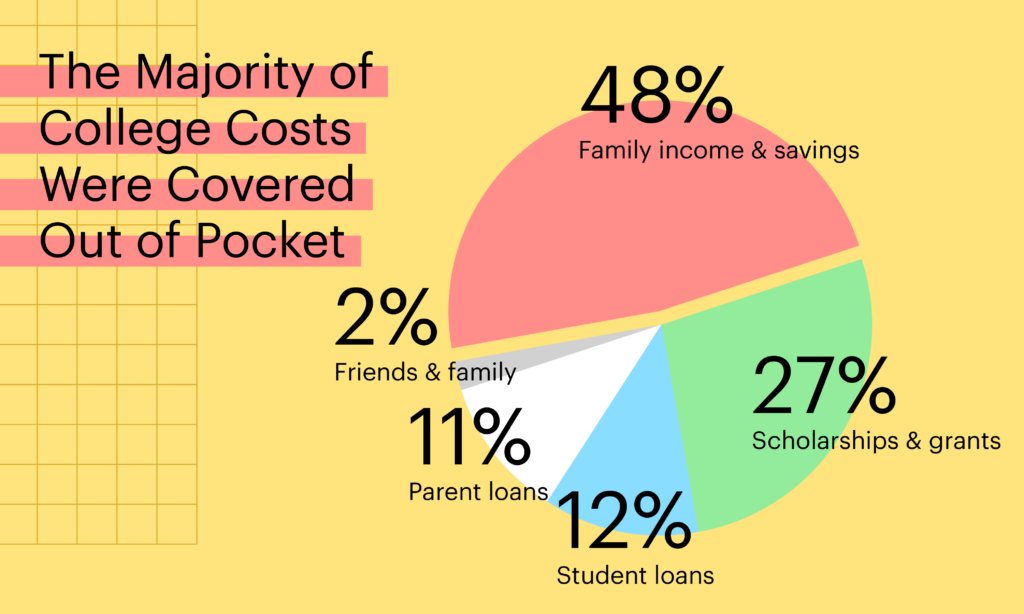

The majority — 48% — of college costs were covered by family income and savings, followed by scholarships and grants (27%), borrowing 23% and funds from friends and family (2%).

Impact of FAFSA® delays

Seventy-four percent of families submitted the Free Application for Federal Student Aid (FAFSA®) for the 2023-24 academic year — marking a steady increase year over year. However, for those who reported completing the new FAFSA for the 2024-25 academic year, just 29% found the new application easier to complete.

Of those who experienced a delay, 44% reported experiencing stress waiting for financial aid decisions, 21% sought out additional financial aid options, 14% considered switching to a lower-cost school, and 10% transferred schools.

Borrowing is up for students and families.

Parents of HBCU students reported significantly higher balances for Federal Parent PLUS loans on average than families at non-HBCU schools: $14,207 vs. $5,795.

Roughly half of students who borrowed (48%) expect their federal loans to be forgiven; Just 40% of families who borrowed discussed who would be responsible for paying back student loans.

Scholarships can drive college access but misconceptions persist.

Scholarships were used by 64% of families, most of whom cited that scholarships made it possible for their students to attend college. On average, families reported receiving $8,250 in scholarships from their schools.

More than half of families (52%), however, believe scholarships are only available for students with exceptional grades or abilities. 50% of families who didn’t apply for scholarships cited lack of awareness.

To connect more students and families to scholarships, Scholarship Search by Sallie easily finds and sorts through hundreds of available scholarships.

Having a plan to pay makes a difference and boosts confidence.

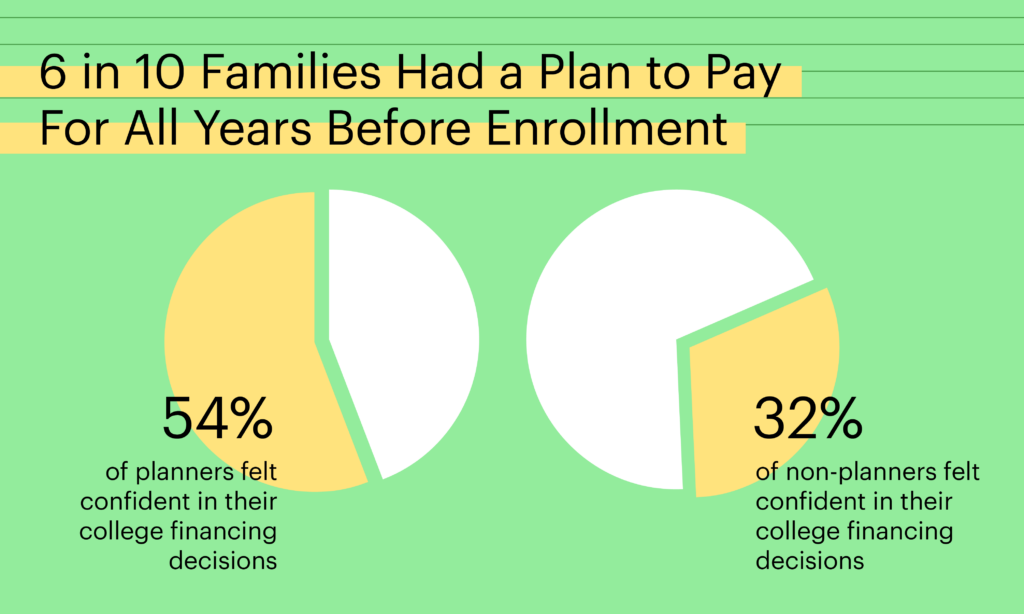

Nearly 6 in 10 (59%) of families had a plan for how to pay for all years of college before enrollment — a more than 10% increase in 5 years — with higher income families more likely to have a plan.

More than half (54%) of planners felt completely confident in their college financing decisions, compared to just 32% of non-planners.

HBCU students agree earning a degree will create more opportunity.

Historically Black Colleges and University (HBCU) families received $14,217 from scholarships and grants. The largest funding source was grants and scholarships, covering 44% of costs while family income and savings covered 29%, borrowed funds covered 26%, and friends and relatives contributed 1%.

88% of HBCU students agree that earning a college degree will create opportunities they wouldn’t have had otherwise, and 81% believe it will translate to a higher earning potential.

These findings confirm families are increasingly recognizing the importance of financial planning for college. That said, the system can be improved by providing more clarity around the actual costs of college, offering greater transparency in federal lending programs, and further connecting students to grants and scholarships.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability