Category: Financial Literacy

09.04.2025

How America Pays for College 2025

Education solutions company and responsible private lender Sallie Mae and research firm Ipsos® recently released its annual research report, How America Pays for College , providing key insights into how current undergraduate students and parents of undergraduates view higher education and how they plan and pay for it. This industry-leading research considers education funding sources — from parent and student income and savings to scholarships, grants, and borrowed funds — while evaluating trends in college spending over time.

Surveyed

1,000 parents of undergraduate students (ages 18–24)

1,000 undergraduate students (ages 18–24)

College Spending Increases

Undergraduate families reported spending an average of $30,837 on higher education for the academic year 2024-25 — a 9% increase from last year’s $28,409. This year’s spending is more in line with 2019–20, pre-pandemic, when families spent an average of $30,017 on college.

Families relied on income and savings to cover nearly half (48%) of costs, followed by scholarships and grants (27%), borrowing (23%), and contributions from family or friends (2%).

Families See Value in College but Remain Cost-Conscious

Nearly nine in ten families (89%) said college is a worthwhile investment, and 82% are willing to stretch their finances to ensure the best opportunities for their students. At the same time, 79% reported eliminating at least one school based on cost. It’s also worth noting that 47% reported paying less than the sticker price for college.

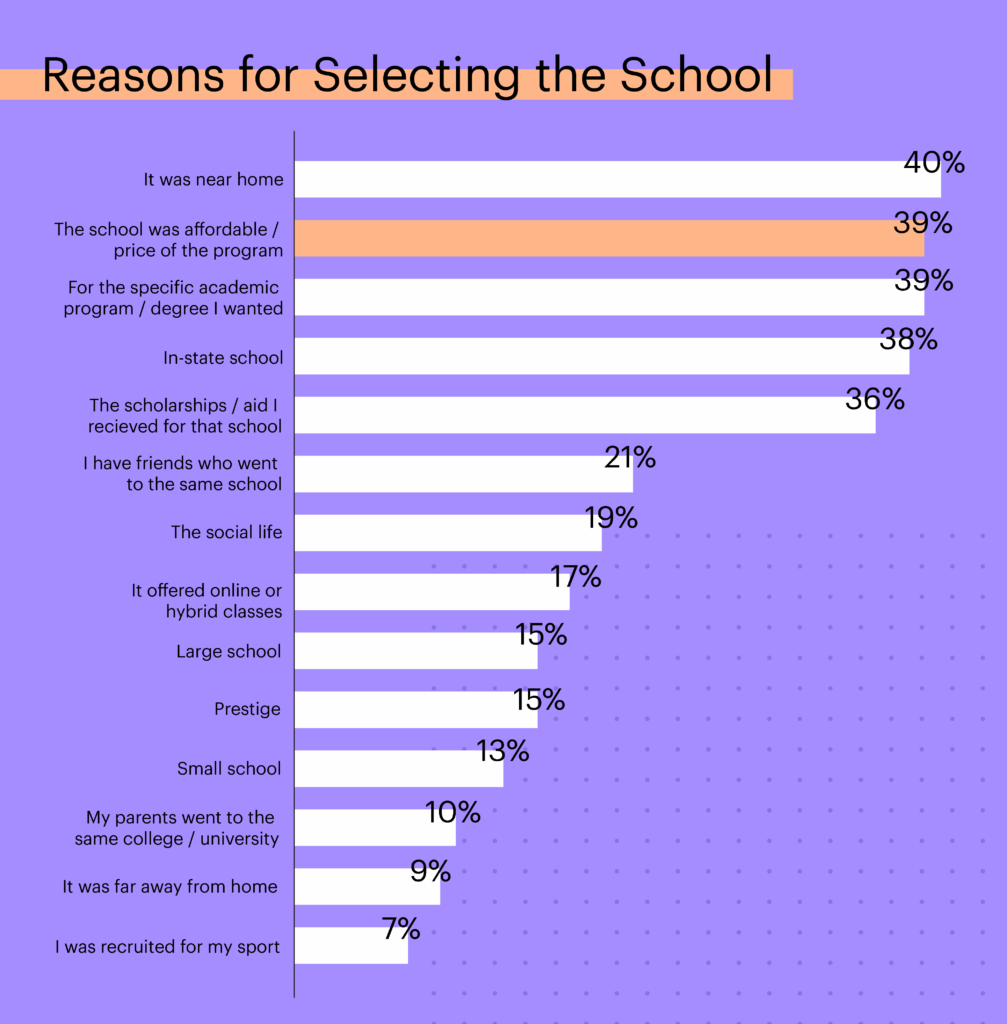

Families most often cited proximity to home (40%), affordability (39%), and specific academic program (39%) as top reasons for choosing a school. While 59% of families had a plan to pay for college before enrollment, just 38% considered starting salaries after graduation.

Key Resource: Find the right college for you

Scout College Search by Sallie® is a free and easy way to explore and compare schools based on location, majors, extracurriculars, and more.

Misconceptions About Scholarships Persist

Scholarships remain a valuable tool to help students and families access higher education. Families who received scholarships reported an average of $8,004 in funding, and 75% said scholarships made it possible for the student to attend college.

Still, misconceptions about scholarships discourage some families from applying. Nearly half of families (46%) believe scholarships are only for students with exceptional grades or abilities, 34% didn’t apply because they didn’t think there were scholarships for them, and 32% assumed it wasn’t worth applying if their family earned “too much.” Another 36% mistakenly thought students could only apply before freshman year.

Key Resource: Search for scholarships

Find free money for college with Scholly® Scholarships by SallieSM, our free tool that connects students and families to thousands of scholarships–no signup required

FAFSA® Completion Declines Despite Easier Form

In academic year 2024–25, the first year that the updated FAFSA was rolled out, 71% of families submitted the application, down from 74% in 2023–24, despite 64% saying the new form was easier to complete.

Confusion remains: only 21% of families knew the FAFSA opens in October.

Families are also looking for clearer, more consistent financial aid communications. Two-thirds (66%) support standardizing financial aid offers to make them easier to compare, suggesting strong demand for clearer, more transparent communication around college costs.

Key Resource: Fill out the FAFSA® with our step-by-step guide

Everything students and families need to get ready for the FAFSA, including a free step-by-step guide that breaks down every question.

Access to Loans Leads Some Families to Reach for Higher-Priced Schools

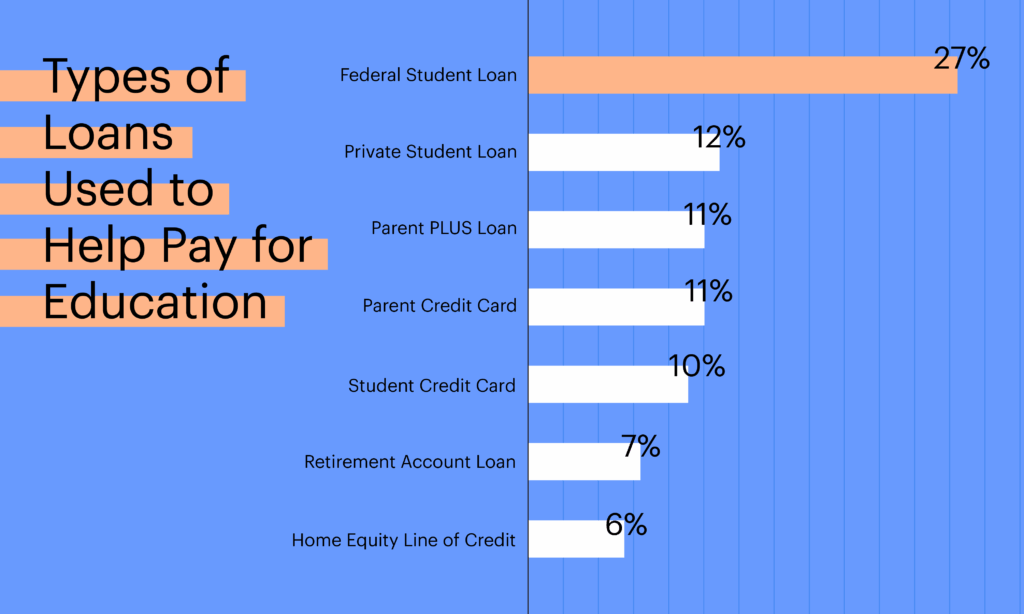

Nearly half of families (48%) borrowed to help pay for college, and 72% of all families said they would rather borrow than miss out on attending. Roughly six in 10 families (59%) said the availability of federal student loans has driven up college costs, and more than a third (35%) of families said loan availability led them to consider more expensive schools. In addition, two-thirds of families (67%) said they support limits on how much federal student loan debt students can take on.

Key takeaways:

This year’s How America Pays for College findings underscore the importance of early planning and starting the higher education journey with outcomes in mind—considering the full picture of education costs and career paths. It also further highlights that many families still miss critical steps that could improve both college affordability and post-graduation success. More broadly, it illustrates the need for more transparency related to college costs, stronger awareness of available aid, and clearer communication around borrowing.

Download the full How America Pays for College 2025 report at SallieMae.com.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

by Nicolas Jafarieh, EVP, Sallie Mae | 06.10.2025

The Federal Government Allows Students and Families to Overborrow to Pay for College. It’s Time to Put an End to It.

The great promise of higher education has always been grounded in opportunity, personal and professional growth, and upward social mobility. Earning a degree equips students with the skills to compete in an evolving economy, increases lifetime earnings, and creates lasting multi-generational impact, especially for those from economically disadvantaged households.

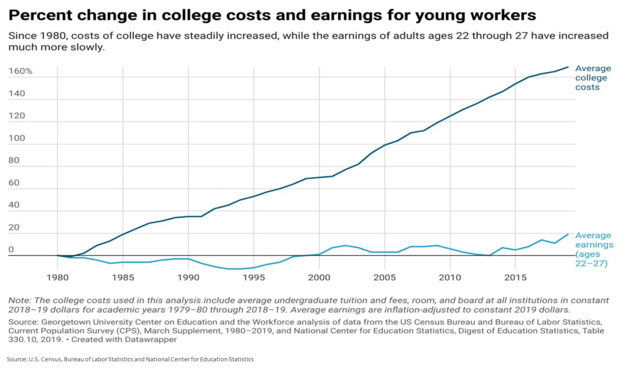

Looking at lifetime earnings alone, the value of a higher education for the vast majority of Americans is undeniable. Sadly, these benefits are slipping away for too many. The cost of attendance is rising more rapidly than wages for college graduates, squeezing the “return on investment” for a degree. Since 2000, tuition at public four-year institutions has surged nearly 180 percent.

SOURCE: U.S. Census, Bureau of Labor Statistics and National Center for Education Statistics

Institutional spending on administrative expansion, facilities, and non-academic programs has led to an ‘arms race’ among schools with costs passed along to students and families, many of whom already struggled to make college affordable. The system also notoriously lacks transparency, ranging from admissions and selection criteria to the real cost of attendance, making it very difficult for families to comparison shop and make informed decisions.

A System That Fuels Rising Costs

The federal loan program, originally designed to provide better access to higher education, has made college less affordable, and ushered in an age of overborrowing. Each year, the government lends more than $80 billion to students and families. Over the last two decades, loan limits have gone up and the federal government allows students and families to borrow more and more, much of it without ever assessing their ability to repay this debt. The Federal Reserve Bank of New York found much of the increases in loan limits directly translated to tuition increases. And these tuition increases, in turn, are forcing students and families to borrow even more.

Federal Graduate and Parent loans are made in virtually unlimited amounts, and again, without any meaningful assessment of the borrower’s ability to repay them. This unconscionable practice has no equivalent anywhere in the financial world. The impact has been staggering. Today, 3.6 million families owe collectively more than $100 billion in Parent PLUS loans. Federal graduate lending has exploded, adding another $100 billion more to the federal balance sheet, accounting for nearly half of all newly issued federal student loans. These programs have been labeled ‘predatory’ from experts on both sides of the aisle, and polling confirms most Americans believe addressing the unlimited nature of federal loan programs will protect students, and make college more affordable. According to the Committee for a Responsible Budget, reforms to graduate lending alone could generate over $40 billion in savings over the next decade—money that could be used to expand Pell grants and need-based aid.

Redirecting Resources to Those Who Need Them Most

Pell Grants, once a cornerstone of college affordability for those who truly needed assistance, haven’t kept pace with rising tuition. They now cover less than 30 percent of the average cost at a four-year public university, down from nearly 80 percent in 1980. Meanwhile, partly the result of missteps like the recent FAFSA delays, more than $4 billion in Pell Grants went unclaimed last year— money that could have helped students who need it most. Increasing Pell Grants for those who need the most support is one of the most effective ways to reduce their reliance on borrowing and keep access to college within reach for all Americans.

Allowing students to use grant aid on non-traditional programs, including short-term job training or apprenticeships, would help more individuals find a long-term path to professional and financial success. A traditional 4-year college continues to be attractive for most, but it is not the right answer for everyone.

Fixing the system, however, isn’t just about shifting resources, it’s also about transparency and ensuring families can make informed choices. College admission is stressful, and offer letters compound the problem. Financial aid offers should be clear, standardized, and easy to compare, giving families the information to make responsible school selections and financial decisions. That is not the case today.

We also need to help more students complete their degree. The great promise of higher education comes not from earning a few credits but from walking across the graduation stage. According to the National Student Clearinghouse, the number of Americans who have some college experience but no degree has now reached a staggering 40 million. Sallie Mae has partnered with Delaware State University to study how near-completer students can be re-engaged and policy solutions that help them complete their degree.

The Need for Reform

By offering federal Graduate and Parent PLUS loans in virtually unlimited amounts, and without considering the borrower’s ability to repay them, the federal government continues to operate like a predatory lender that saddles families with unsustainable levels of debt. This isn’t a failure of students and families—it is a failure of policy. Without meaningful reform to curb overborrowing, the cost of college will keep rising, another generation of students will keep taking on unaffordable debt, and taxpayers will keep footing the bill.

The solutions exist. Now is the time to act.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

05.13.2025

Supporting Students from Dream to Degree: Sallie Mae’s Commitment to College Completion

In 2023, Sallie Mae underscored its commitment to closing the college completion gap with a $1 million research endowment to Delaware State University (DSU). The grant supports a “Persistence and Completion Pilot Program,” that identifies and studies barriers to degree completion, helps students return to school, and develops policy recommendations and best practices so students can re-engage at institutions across the country. To date, the program has re-enrolled 213 students — nearly half of them first-generation college students.

This is important work. The number of students who have some college experience, but no degree, is over 40 million. Approximately 3 million are “near completers” who have stopped out mere credits away from degree completion.

Two near completer students — Nataniel (Tannie) Speaks and Chris Kearney — are proof of what’s possible when students get the right support at the right time.

After earning an associate degree, Tannie hoped to continue her education — but full-time work and raising two children put that goal on hold. Years later, she learned about the near completer program and re-enrolled at DSU. Five months later, she earned her bachelor’s degree.

“I still get chills and tears just thinking about it,” she said.

Chris’ journey also spanned decades. He first enrolled at DSU in 2000 with plans to earn a history degree, but stepped away in 2005 to support his growing family. A decade later, when his mother was diagnosed with breast cancer, Chris was determined to finish school for her. But after her passing, he once again put his education on hold.

In 2022, Chris felt a renewed urgency. “I’d reached a certain point in my career path where I felt the need to have my degree completed,” he said. “I thought it would complete me more holistically and professionally.”

In 2023, he graduated with a degree in liberal studies — this time, with his wife, siblings, and children cheering him on. “It felt like I was showing and giving examples to my children about fortitude and perseverance, about how sometimes when life happens, you can transcend, you can overcome and you can change the trajectory of your life for the better,” Chris said.

For Tannie, the impact of earning her degree was immediate.

“I want everybody—kids, young people, old people—to know that it’s never too late to finish your education,” Tannie said. “It’s a second chance at making something new.”

“Reach out to Sallie Mae. They have resources, they have things at their disposal to help encourage you to come back, and not only encourage you to come back, help you see this through to the end of your journey, ” Chris said. “You can do it. You have the wherewithal. You have the grit. Get it done.”

Sallie Mae is committed to supporting college completion. Too many students leave school just a few credits shy of a degree — often due to financial strain or personal circumstances. In fact, our 2024 “How America Completes College” report found that nearly half of non-completer said financial challenges played a role n their decision to leave school. Through programs like the “Persistence and Completion Pilot Program” at Delaware State University — and our “Completing the Dream Scholarship” — we’re helping remove barriers and support more students from dream to degree.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

11.22.2024

FAFSA: The Quiz

Each year, millions of students and families begin planning for college by completing the Free Application for Federal Student Aid (FAFSA®). It’s the gateway to accessing more than $100 billion in grants, scholarships, and other federal financial aid for higher education. Confusion and misconceptions about the FAFSA, however, persist — leading those who need the most support to potentially miss out on critical aid to make college more accessible and affordable. As an education solutions company and responsible private lender, Sallie Mae helps students and families complete the FAFSA, offering a free step-by-step guide as well as free resources to connect them to scholarships.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

11.22.2024

Why Scholarships are Critical for Families Paying for College

Paying for college can be a complex, stressful process. Yet, a new study finds students and families may be missing out on scholarships, which can help make college more accessible and affordable. In fact, 40% of families did not utilize scholarships to help cover college costs for the 2024-2025 academic year, according to Sallie Mae’s 2025 How America Pays for College report conducted by Ipsos.

In addition, misconceptions about scholarship availability and eligibility persist. More than half of families (52%) believe scholarships are only available for students with exceptional grades or abilities, and families who didn’t apply cited lack of awareness, doubt in winning, and effort required to apply. Families who didn’t apply cited lack of awareness (34%), doubt in eligibility (28%), and the effort required to apply as barriers.

The good news is there are free resources that can help connect students and families to scholarships. Scholly Scholarships easily finds and sorts through hundreds of available scholarships with no registration required.

Don’t Leave Free Money on the Table

Applying for free money is the first step in Sallie Mae’s 1-2-3 approach to paying for college.

Free money, such as scholarships and grants, are often what helps students from underserved communities access and complete higher education.

To help increase access and completion for more students, Sallie Mae’s Bridging the Dream Scholarship Program helps those from underserved communities access and complete college. Since 2021, Sallie Mae has awarded over 1,100 scholarships worth over $4 million in partnership with Thurgood Marshall College Fund (TMCF) through the Bridging the Dream Scholarship programs, which also include the Completing the Dream Scholarship and the Bridging the Dream Scholarship For Graduate Students. These scholarships are part of the company’s continued mission to help students access and complete higher education.

Connecting students with scholarships and grants before they borrow is critical. However, more clarity around college costs and greater transparency in federal lending programs would go a long way in helping families make informed decisions about higher education financing.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

08.19.2024

What Students and Families Need to Know About The FAFSA

As a responsible private lender, Sallie Mae advises students and families to explore free money like scholarships and grants before borrowing. The gateway to this aid is the Free Application for Federal Student Aid (FAFSA®), which gives students and families access to $114 billion in scholarships, grants, state-based and federal financial aid. Too many families, however, miss out on this critical aid because of persistent misconceptions about their eligibility or confusion around how to complete the application, resulting in billions of dollars left unclaimed each year.

This year saw significant glitches and delays resulting from the rollout of a new FAFSA with fewer questions. While the intent was to streamline and simplify the process and expand eligibility for need-based aid like Pell grants, persistent implementation issues left students and families frustrated and financial aid offers from schools delayed.

About 74% of families reported completing the FAFSA for the 2023-2024 academic year, according to Sallie Mae’s How America Pays for College 2024 report. Of the families who filled it out for the 2024-2025 academic year, only 29% found it easier to complete. In addition, of those who experienced a delay, 44% reported experiencing stress waiting for financial aid decisions and 21% sought out additional financial aid options. When it comes to financial aid offers from schools, 71% of families said they support a simplified, standardized letter. Despite the FAFSA confusion, 88% of families still believe college is an investment in their child’s future, and 79% are willing to stretch financially to get there.

While these delays point to broader issues with the federal financing system for higher education, it’s still critical for families to complete the FAFSA. The FAFSA® is an important first step for students and families to help make college more accessible and affordable. Sallie Mae supports simplification of the FAFSA® and is improving awareness to help more students and families connect to scholarships, grants, and other critical aid.

As an education solutions provider, Sallie Mae provides free tools including a step-by-step FAFSA guide, information, and webinars to help students and families navigate the new FAFSA and complete it. We also offer free resources like Scholarship Search by Sallie to help students and families find and apply for scholarships.

Here are five important points that students and families should know about the FAFSA®:

1. All students—regardless of family income—should complete the form.

Most families—87%—know to submit the FAFSA® each year so that their student qualifies for financial aid, but not all families know that every student is eligible to apply. Some 33% of families believe their income is too high for their student to qualify for aid, the most frequently mentioned reason why families didn’t submit the FAFSA® last year.

The reality is all students, regardless of income, should complete the form. Some of that aid, like scholarships, grants and state-based aid, is offered on a first-come, first-served basis. That’s why the sooner families can complete the FAFSA®, the better. Rollout for the FAFSA will start October 1st and the form will be fully available on December 1st for the 2025-2026 school year.

2. The FAFSA® is free.

Families should never pay to submit the FAFSA®. Filing is free, period. A paid service will not get students more aid. Sallie Mae offers students a step-by-step guide for navigating the new FAFSA, but they can also check with their high school, local college, and financial aid office for assistance.

3. Fill out the “special circumstances” form when financial information changes.

Students and families—including those attending graduate school—should complete the FAFSA® every year they are in school. That said, sometimes income and other factors may change due to circumstances such as a job loss or medical emergency. That’s when completing a “special circumstances” form may make sense. The form is available from college financial aid offices and can help students receive additional aid in certain situations.

4. List schools on the FAFSA® even if it’s not a final list.

If students don’t list all colleges they’re considering on their FAFSA®, then the schools won’t know the student is interested in applying for grant money from them. Students should also always list state schools first in case they offer additional state-based aid on a priority basis.

5. There is no age limit.

Federal financial aid is just as available to non-traditional students in the 24- to 35-year-old range as it is to students in their late teens and early twenties. There’s no age limit for receiving federal financial aid—so all students and families should apply.

FAFSA is a registered service mark of U.S. Department of Education, Federal Student Aid

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

05.22.2024

How Sallie Mae Prepares Students to Pay Back Their Loans

After years of studying and working hard, millions of college graduates across the nation are transitioning from college to the next chapter of their lives. This could mean new jobs, new cities, or new goals — a cause for celebration.

Even after students finish college, the learning doesn’t stop. Next on the syllabus is setting and maintaining a healthy budget, and for those who borrowed to pay for college (41% of students, according to our “How America Pays for College 2023” report), that budget will soon include paying back student loans.

To ensure students get started on the right track, Sallie Mae® works to remove the element of surprise from loan payments by initiating clear communication with students and cosigners while they’re in school and throughout the life of their loans. As a responsible private lender, we believe that transparency and clarity about how much students and families owe and when they need to pay back their loans is critical to helping them responsibly plan for higher education.

Staying up to date on student loan status

Students have very busy schedules, which is why we make it as easy as possible for them to stay up to date on the status of their loans. Students can create an online account or download the Sallie mobile app to get notifications of when their upcoming payments are due. They can even enroll in auto-debit to ensure their payments are always on time, which can also save them money by lowering their interest rate.

We also send students and their cosigners a loan summary each year they are in school, including interest accrued. This is especially important for customers who choose to defer payments on their loan during college, as it helps them keep track of what they’ve borrowed and what they owe. That said, roughly half of our customers choose to make a fixed payment or pay interest on their loans while in school, which can significantly lower the total cost of the loan.

Tools and tips for the six-month separation period

Sallie Mae private student loans come with a six-month separation or grace period for undergraduate programs that begins once a student leaves school, giving them time to find a job and get settled into post-college life. We let students know at the start of their grace period what their estimated payment amount will be and provide tips on when, where, and how to pay on time.

We also offer free tools to help students prepare for repayment, such as a monthly budget worksheet, which helps students create a budget to meet their financial goals and our student loan repayment calculator that gives students an estimate for their upcoming monthly payments.

At the end of the day, preparation is key to responsible financial planning. From the moment students take out a loan through the months post-graduation, we help students and families not only meet their loan payments, but make strides toward their financial goals.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

08.15.2023

5 Things to Know About How America Pays for College

The federal higher education financing system is complicated and can often leave families feeling confused about all the potential paths for their education journey and where to start. To better understand how students and parents approach planning and paying for college, Sallie Mae annually conducts its “How America Pays for College” report with Ipsos.

The research explores education funding sources—from family income and savings to scholarships, grants, and borrowed funds—and evaluates trends in payments over time.

Here are five things to know about how America pays for college:

1. Slightly more than half of families have a plan for how to pay for college.

Last year, 53% of students and families reported making a plan for how to pay for college before the student enrolled, slightly down from last year’s high of 59%.

Students attending four-year public and private schools are more likely to plan ahead than students attending 2-year schools. The same goes for families with prior college experience. Fifty-five percent of families with college experience have a financial plan, compared to 45% of first-generation college families.

An even larger gap exists between higher- and lower-income families. Seventy-nine percent of families who make more than $150,000 per year had a plan, compared to just 43% of families who make less than $50,000.

Sallie Mae helps power confidence through free tools like Scholarship Search by Sallie, where students can easily access a wide variety of scholarships.

2. Majority of families are still unaware of when the FAFSA® becomes available.

While FAFSA completion rates are holding steady at 71%, just more than seven in 10 families are still unaware of when the application opens, and 30% of families bypass the form altogether.

Among the families who didn’t submit the FAFSA, majority believed they made too much money to qualify. Twenty-five percent of families found the application to be too complicated, while nearly 30% reported not having the required information for the application.

The FAFSA is the gateway to accessing more than $112 billion in grants, scholarships, and federal financial aid for college, and those most likely to qualify for aid are not completing the form due to lack of awareness. States and colleges rely on information from the FAFSA to determine need-based aid for qualifying students.

3. Scholarships are key for accessing higher education, especially for students attending HBCUs.

Scholarships play a meaningful role in families’ college journeys—not only as a source of funding —but also a source of pride. More than half — 61% — of families relied on scholarships to help lower the cost of college last year. Most scholarships were given from the school the student was attending, followed by the state and non-profits or organizations.

For families who didn’t take advantage of applying for scholarships, most said it was due to lack of awareness, low confidence in winning, or common misconceptions about who is eligible to apply. Forty-five percent of students and parents believe scholarships are only for exceptionally gifted students. In fact, there are scholarships available for all types of students — from being a first-generation college student to being left-handed.

Sallie Mae helps connect students to scholarships through Scholarship Search by Sallie.

4. Many families eliminate schools based on cost.

Choosing a college is a momentous decision that is largely impacted by the cost of attendance. Seventy-eight percent of families eliminated a school based on cost at some point during their college search and decision process last year. Around one third of families — 32% — said the current state of the economy impacted their decision as well.

Yet, 75% of families said they were willing to stretch themselves financially because they view higher education as an investment in the student’s future.

Sallie Mae helps students and families finance their higher education responsibly by encouraging and educating students on utilizing scholarships, grants, and other federal aid before borrowing.

5. Many lower-income and first-generation families rely on grants.

While 57% of all families used grants to pay for college last year, first generation families and families earning less than $50,000 per year — 68% and 74% respectively — reported higher grant usage.

Sallie Mae supports meaningfully expanding grants, such as the Pell Grant — which has helped more than 80 million low-to middle-income students access and complete higher education. Last year, around $3.6 billion in Pell Grants went unclaimed, aid that could have helped more students achieve their college dreams. Meaningful reforms, such as the FAFSA Simplification Act and increasing the maximum Pell Grant amount, could help more students access this critical aid.

FAFSA is a registered service mark of U.S. Department of Education, Federal Student Aid

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

02.08.2023

POP Quiz: How much do you know about higher education financing?

College should be more affordable and accessible for students from all backgrounds, and we’re committed to making that happen by helping families confidently navigate to, through and immediately after college. We power confidence in students and families by providing tools and resources to make informed decisions about higher education.

Test your own college preparedness knowledge by taking the quiz below.

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability

02.01.2023

Sallie Mae’s 1-2-3 Approach to Paying for College

Figuring out how to pay for higher education can be stressful and complicated. Follow our three-step approach to simplify the process:

1. Start with money you don’t have to pay back.

Consider any savings or income you can put toward your tuition.

- Savings: In addition to tapping current income, consider a tax-advantaged account like a 529 plan or goal-based savings account that can be used to cover education costs.

- Scholarships: Millions of scholarships are available for incoming and current college students. Sallie Mae’s free Scholarship Search Tool can help you find the scholarships best suited for you.

- Grants: Colleges, states, and the federal government provide funds to students based on need. Complete the Free Application for Federal Student Aid (FAFSA) early to maximize your chances of receiving grants.

- Work-study: These part-time jobs allow students to earn income while in school. Make sure to submit your FAFSA to be considered for work-study programs.

2. Explore federal loans.

Federal loans are made by the government, available to everyone without assessment of ability to pay them back, are taxpayer funded, and most need to be paid back with interest. Students can apply by completing the FAFSA.

3. Consider a responsible private loan.

Private student loans can bridge the gap between income and savings, scholarships, grants, federal aid, and any remaining higher education costs.

Private student loans are credit-based and underwritten, meaning the lender assesses the student’s ability to afford a loan before approving it.

Because most students do not have significant credit profile, majority of private student loans require a cosigner to qualify.

Like the majority of federal student loans, private student loans need to be repaid with interest.

Borrow responsibly

Sallie Mae encourages students and families to start with savings, grants, scholarships, and federal student loans to pay for college.

For more information, visit SallieMae.com/CollegePlanning

Related Posts

Who Sallie Mae Is — and Isn’t

Accountability